Combined finances could accelerate wealth accumulation given that both parties in the marriage have common financial goals. Also, combined financial power can contribute to a sense of solidarity, as you begin to think of spending as a unit. Saving together allows a couple to start working towards mutual goals, such as buying a house, going on an overseas trip or building passive income.

On the other hand, separate finances will be a fairer system if the couple have a huge income disparity or markedly different spending habits. Also, it may allow greater independence when it comes to spending and make personal gifts and dates more special.

What appeals to me most is a hybrid system that incorporates the benefits of both combined and separate finances. In this system, both spouses put their entire paycheck into the joint account, and then withdraw a fixed amount(allowance) into their personal accounts every month. Household expenses and bills will be deducted from the joint account.

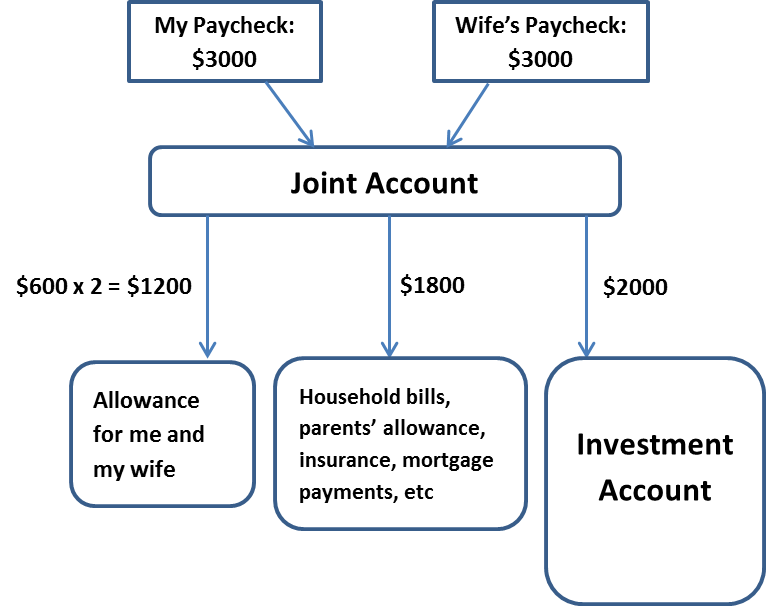

Below is an illustration of the system assuming take-home pay to be $3,000 each:

Both my wife and me will deposit our entire paychecks into a joint account. We will each withdraw $600 as our allowance. If there is any amount left at the end of the month, we will deposit into our personal accounts and this will form our individual personal savings. Parents' allowance, household bills, insurance, cash portion for mortgage payments and other miscellaneous expenses will be debited directly from the joint account. Also, an amount of $2,000 will be set aside every month as our opportunity fund. There will be a leftover of $1,000 in the joint account every month and this will be our combined savings/emergency fund.

Tidak ada komentar:

Posting Komentar